Major upcoming global economic releases and events

| Date | Data / Event | Previous | Consensus |

| 31-May-22 | Australia building permits m/m (Apr) | -18.5% | 2% |

| 31-May-22 | Australia private sector credit m/m (Apr) | -0.4% | NA |

| 31-May-22 | Europe core inflation y/y (May) | 3.5% | 3.5% |

| 1-Jun-22 | Australia GDP growth q/q (Q1) | 3.4% | 0.7% |

| 3-Jun-22 | Australia home loans m/m (Apr) | 0.9% | -1% |

| 3-Jun-22 | Europe retail sales m/m (Apr) | -0.4% | 0.4% |

| 3-Jun-22 | US unemployment rate (May) | 3.6% | 3.5% |

Source: Bloomberg, UBS Global Research, Tradingeconomics.com

What to watch this week

| Australia | US | Europe |

|---|---|---|

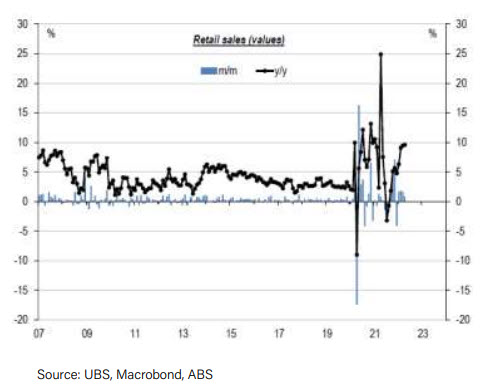

| Domestic data was mixed last week, with Q1 GDP partials and May PMIs weaker than expected, but retail sales posting another solid gain in May. Q1 GDP numbers will be published this week and the partial data released so far has been underwhelming. Both construction and capex data were weaker than expected in Q1, with both series registering negative numbers that were close to 2% below consensus. Covid-related disruption, and impacts from significant rain events suggest that the Q1 release could be soft this week. While Q1 may end up being weaker than expected, the domestic outlook remains strong. High commodity prices will provide a benefit to the domestic balance sheet, while the removal of mobility restrictions combined with pent up demand, high saving rates and a tight labour market should more than compensate for fears around rising interest rates. In addition to the GDP print, building permits, private sector credit and home loan data are all due to be published in a busy week ahead. | US PMI data showed surprising weakness in the services sector in May, in a reversal of the recent strengthening trend. Other business surveys also pointed to slower activity in the period ahead and the durable goods order print was also weaker than expected in April. The minutes from the recent Fed meeting were published last week, detailing that the 50bp hike was a unanimous decision and also showing that most participants thought that similar moves would be required over the coming meetings. Overall, discussion was focussed on concerns around the inflationary environment, the tight labour market and the need to rapidly increase rates toward neutral levels. The minutes support the view that there is little appetite for 0.75% rate hikes, but the key question from here is when the Fed will be prepared to slow the pace of hikes, and whether they will move beyond a neutral stance. The week ahead sees a number of manufacturing indices and consumer sentiment data set for release ahead of non-farm payrolls, which is the highlight. | UK PMI data was a large underperformer relative to peers in May, with the headline index falling from 58.2 to 51.8. The European series edged lower from 55.8 to 54.9. A relatively calm period in UK politics was interrupted last week by the report into allegations that Boris Johnson hosted parties at his Downing Street residence while the country was under strict lockdown conditions. The report highlights a number of gatherings attended by senior and junior government officials alike and outlines a leadership failure at the highest levels of the UK government. While the public been scathing, senior lawmakers have so far stood by their leader, who became the first British prime minister ever found to have broken the law while in office when fined earlier this year by the are gaining momentum once again. European inflation and retail sales are the key releases this week. |

Chart of the week—Australian retail sales

| INDICATOR | AS AT 27-MAY-22 | 1 WEEK CHANGE | 1 YEAR CHANGE | 3 YEAR CHANGE (ANNUALISED) | 5 YEAR CHANGE (ANNUALISED) |

| EQUITIES | % | % | % | % | |

| S&P/ASX 200 Index | 84,685.45 | 0.55 | 4.16 | 7.73 | 8.78 |

| US S&P 500 Index | 8,766.83 | 6.62 | 0.32 | 16.17 | 13.52 |

| EURO STOXX | 901.56 | 3.82 | -3.46 | 7.69 | 4.30 |

| UK FTSE 100 Index | 7,644.23 | 2.67 | 12.07 | 5.41 | 4.09 |

| Japan TOPIX Index | 2,856.09 | 0.53 | -1.15 | 9.34 | 5.75 |

| MSCI World ex-Australia Index | 6,617.89 | 5.29 | -1.35 | 12.83 | 10.12 |

| FIXED INCOME | % | BP | BP | BP | BP |

| Australian 90 day bank bill yield | 1.13 | 8.38 | 108.88 | -10.20 | -12.16 |

| Australian 10 year bond yield | 3.26 | -5.80 | 162.50 | 56.51 | 16.84 |

| US 90 day bank bill yield | 1.03 | 4.61 | 102.84 | - 42.50 | 2.65 |

| US 10 year bond yield | 2.74 | -4.33 | 113.16 | 13.90 | 9.81 |

| UK 10 year bond yield | 1.92 | 2.40 | 110.70 | 31.93 | 18.03 |

| German 10 year bond yield | 0.96 | 1.90 | 113.50 | 36.76 | 12.61 |

| COMMODITIES | % | % | % | % | |

| Gold | 1,853.72 | 0.39 | -2.26 | 12.98 | 7.91 |

| Oil West Texas Crude | 115.07 | 1.63 | 72.13 | 25.20 | 18.24 |

| Iron Ore Spot Price Index | 134.05 | -0.18 | -34.61 | 10.63 | 17.15 |

| CURRENCIES% | % | % | % | % | |

| AUD:USD | 0.72 | 1.72 | -7.41 | 1.16 | -0.76 |

| EUR:USD | 1.07 | 1.64 | -12.19 | -1.19 | -0.78 |

| GBP:USD | 1.26 | 1.11 | -11.21 | -0.02 | -0.35 |

| USD:JPY | 127.08 | -0.63 | 15.97 | 5.06 | 2.69 |

| NZD:USD | 0.65 | 2.27 | -10.06 | 0.14 | -1.51 |

| CHF:USD | 1.04 | 1.83 | -6.09 | 1.74 | 0.42 |

| AUD:EUR | 0.67 | 0.05 | 5.44 | 2.38 | 0.01 |

| AUD:GBP | 0.57 | 0.69 | 4.30 | 1.19 | -0.41 |

| AUD:JPY | 91.01 | 1.06 | 7.38 | 6.28 | 1.91 |

*BP = Basis Point, Source: Bloomberg; ^TR = Total return.

IMPORTANT NOTE This document has been prepared by Crestone Wealth Management Limited (ABN 50 005 311 937, AFS Licence No. 231127) (Crestone Wealth Management). The information contained in this document is of a general nature and is provided for information purposes only. It is not intended to constitute advice, nor to influence a person in making a decision in relation to any financial product. To the extent that advice is provided in this document, it is general advice only and has been prepared without taking into account your objectives, financial situation or needs (your Personal Circumstances). Before acting on any such general advice, we recommend that you obtain professional advice and consider the appropriateness of the advice having regard to your Personal Circumstances. If the advice relates to the acquisition, or possible acquisition of a financial product, you should obtain and consider a Product Disclosure Statement (PDS) or other disclosure document relating to the financial product before making any decision about whether to acquire it.

Although the information and opinions contained in this document are based on sources we believe to be reliable, to the extent permitted by law, Crestone Wealth Management and its associated entities do not warrant, represent or guarantee, expressly or impliedly, that the information contained in this document is accurate, complete, reliable or current. The information is subject to change without notice and we are under no obligation to update it. Past performance is not a reliable indicator of future performance. If you intend to rely on the information, you should independently verify and assess the accuracy and completeness and obtain professional advice regarding its suitability for your Personal Circumstances.

Crestone Wealth Management, its associated entities, and any of its or their officers, employees and agents (Crestone Group) may receive commissions and distribution fees relating to any financial products referred to in this document. The Crestone Group may also hold, or have held, interests in any such financial products and may at any time make purchases or sales in them as principal or agent. The Crestone Group may have, or may have had in the past, a relationship with the issuers of financial products referred to in this document. To the extent possible, the Crestone Group accepts no liability for any loss or damage relating to any use or reliance on the information in this document. This document has been authorised for distribution in Australia only. It is intended for the use of Crestone Wealth Management clients and may not be distributed or reproduced without consent. © Crestone Wealth Management Limited 2022.

.png?width=770&height=577)