Since late last year, we’ve held the view that central bank policy rates would be trimmed from mid this year. Markets have vacillated from over-exuberance (and an earlier start to rate cutting) to their recent despair (that lower rates will be a 2025 event). Yet, while the sequence of central banks has likely changed—with Europe to lead instead of the US—recent renewed softer inflation and weak non-US growth now see policy easing coming imminently into view. Reflecting this, we edge tactically overweight equities this month to harvest returns as rates fall. Still, fixed income remains our largest overweight for now.

We also take the opportunity to discuss our recent annual investment strategy review, in particular, highlighting our new proprietary multi-asset risk factor framework, which now underpins our in-house strategic asset allocation. We also incorporate our belief that the imperative for nations to compete geo-politically, address societal inequities, and fund the energy transition will underpin a higher resting rate for growth, inflation, and rates going forward. This likely fosters more volatility and dispersion. Reflecting this, our new strategic asset allocations embody, among other things, higher allocations to cash and alternatives, a tailored approach to fixed income, and a renewed strategic equity allocation to Japan.

Over the past month or so, there have been five key global macro developments which support our desire to remain overweight fixed income relative to equities. They also support our decision this month to add near-term risk to portfolios via a modest equity overweight, as well as our preference for domestic equities (and closure of our European underweight).

Global growth—uneventful outlook? Mild slowing then patchy recovery ahead

Recent developments also support our decision this month to add risk to portfolios via a modest equity overweight, as well as our preference for domestic equities (and closure of our European equity underweight).

4. China hits the panic button over property—Despite stronger-than-expected growth in Q1, signs of a loss momentum through the quarter ultimately culminated in a worse-than-expected set of activity data for China in April. The property downturn, in particular, has deepened. In mid-May China’s authorities responded, announcing significant policies to stabilise the housing sector. At the margin, this is a positive development for Australia.

5. Australia consumer slows ahead of budget stimulus relief—Recent weak retail data, together with anecdotes from retailers and banks (where loan arrears have been rising), suggest that high interest rates are now starting to cause stress for consumers. There are also increasing signs that prior labour hoarding is now giving way to job losses. We expect this to reverse recent inflation pressure, with a start to a modest rate-cutting cycle from Q4. While May’s stimulatory federal budget has likely ensured a delay in the timing of rate cuts, we also expect mid-year stimulus to stabilise the economy through H2 2024 and into 2025.

The world around us is changing significantly, from the ongoing uncertainty of twin wars, to the return of state-directed industry policy and ever-increasing capital being deployed globally to the energy transition and AI…

…over the past six months, these forces have been front of mind as we conducted our 2024 review of investment strategy and asset allocation.

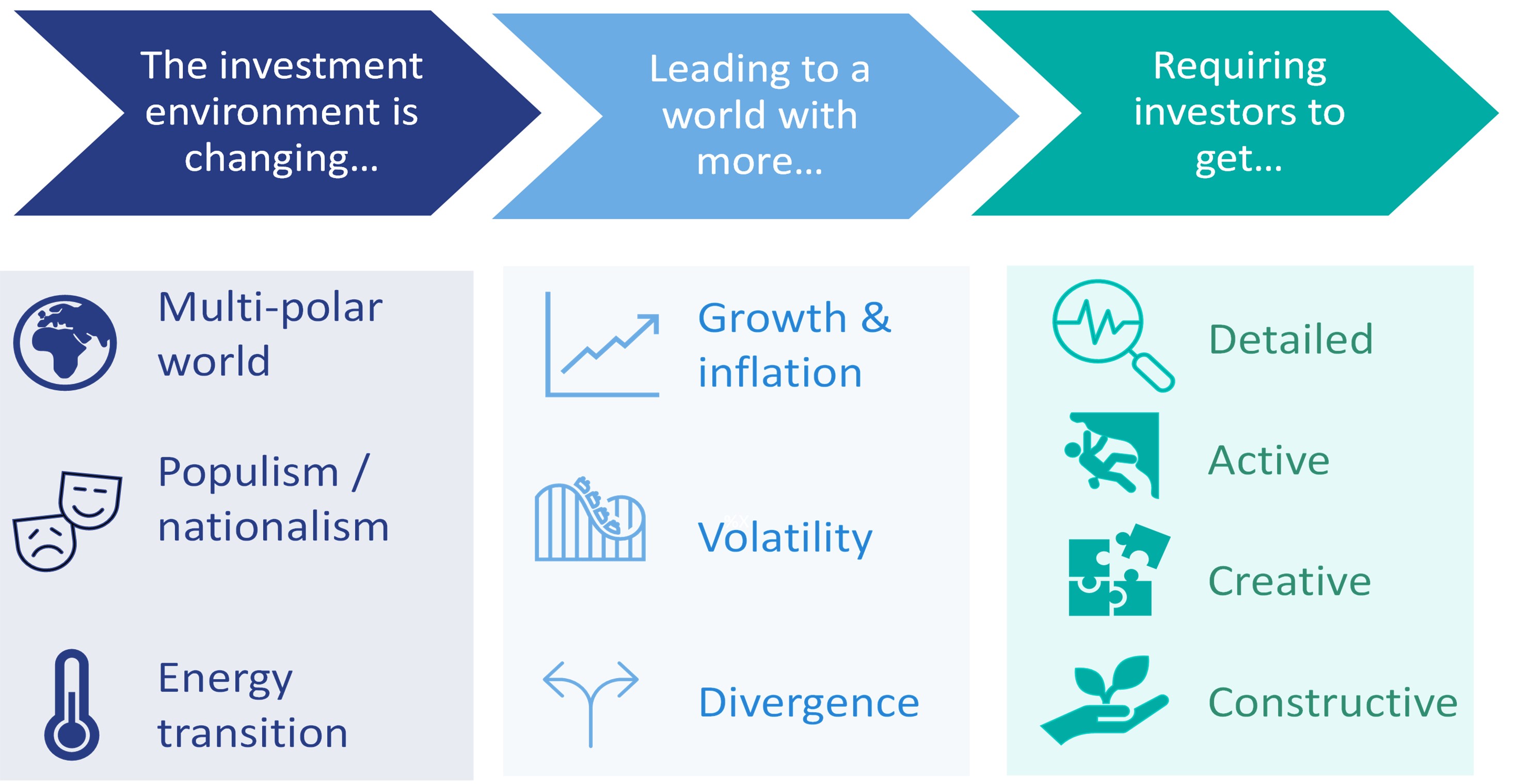

The world around us is changing significantly. Newspaper headlines from just the last few months highlight the ongoing uncertainty of twin wars in Ukraine and the Middle East and the return of state-directed industrial policy (headlined by the US Inflation Reduction Act and, locally, the Future Made in Australia initiative). These come amid increasingly strained social and political cohesion across many developed nations. We are also seeing increasing sums of money being deployed to the energy transition and generative artificial intelligence (AI).

We’ve been studying and assessing these trends for some time. We introduced a framework for considering these evolving structural forces and their implications in our October 2023 Observation titled Asset allocation in a changing world. Over the past six months, these forces and their impact on our long-term secular outlook have been front of mind as we conducted our 2024 review of investment strategy and asset allocation.

The imperative for nations to compete geo-politically, address societal inequities, and fund the energy transition are likely to underpin a higher resting rate for economic growth, inflation, and policy rates going forward.

To briefly summarise our updated secular outlook:

Investment strategy review—our secular outlook

We believe the astute investor can navigate, and even thrive, in this new world. But this will require investors to become more detailed, more active, more creative and more constructive.

Each of these structural shifts is likely to be incredibly impactful for the global economy and financial markets in isolation. Taken together, we see complex interactions between them that are likely to intensify their collective impact on the investment environment:

While our outlook might appear to paint a troubling picture for portfolios, we believe the astute investor can navigate, and even thrive, in this new world. However, as discussed in our October 2023 Observation, this will require investors to become more detailed, more active, more creative, and more constructive as they outwork their investment strategy.

We have introduced a proprietary multi-asset risk factor framework that now underpins our in-house capital market assumptions.

As part of embedding these four actions across our 2024 investment strategy review, we have introduced a proprietary multi-asset risk factor framework that now underpins our in-house capital market assumptions (i.e., the risk, return and correlation assumptions we make across all our asset and sub-asset classes). This framework traces its roots to the 1970s and builds on a multi-decade journey driven by some of the investment world’s great pioneers, including Markowitz, Sharpe, Treynor, and Fama and French.

The theory rests on several underlying beliefs:

This approach gives us powerful tools to better understand asset class behaviour and portfolio design. In the first instance, our deeper understanding of risk and return can help us better compare asset classes across a level playing field. For example, if we believe that interest rates have peaked and will fall, we can deliberately calibrate our preferences across asset classes that have a strong exposure to falling interest rates, such as government bonds, credit, or infrastructure.

At a total portfolio level, we can now also estimate a total multi-asset portfolio’s sensitivity to equity risk or interest rates, and better monitor that portfolio’s exposure. This is a key risk management tool employed by some of the most sophisticated institutional investors, including the Future Fund.

We can now estimate a total multi-asset portfolio’s sensitivity to equity risk or interest rates. The former is a key risk management tool employed by some of the most sophisticated institutional investors.

This enhancement to our strategic asset allocation (SAA) process has allowed us to conduct a deep review of the investment strategies across our model risk profiles, which are laid out below and encompass the following improvements:

We believe that these changes to our SAAs, alongside the improved analytical tools that our proprietary multi-asset risk factor framework gives us, will allow our clients to best adapt to, and take advantage of, the changing investment environment.

Our updated SAAs embody a small upward adjustment to cash weightings, a more customised approach to fixed income across risk profiles, a new Japan equity allocation, and a larger allocation to alternatives.

For most of the first half of this year, we have communicated a constructive tactical positioning for portfolios. This has been characterised by an underweight position to cash, deployed into an overweight in fixed income. We also retained a neutral exposure to equities to balance, at times, challenging valuations with an expected more supportive outlook embodying lower interest rates and a ‘softish’ economic landing.

This month we are adding some risk, moving modestly overweight equities. As discussed in our May 2024 Observation: Building better portfolios—An evolution of the 60/40 portfolio, periods of elevated inflation tend also to be periods where equities and fixed income returns are positively correlated. While a renewed outbreak of inflation and shift to further monetary policy tightening could lead to weakness across both traditional asset classes, our greater confidence that inflation and rates are moderating for a time supports modest gains across both. If risks of a hard economic landing were to re-emerge, our overweight to fixed income would also provide some downside protection to portfolios.

Cash (Underweight -3)—We retain an underweight cash position. We believe cash rates have peaked and returns will moderate as interest rates in Australia are trimmed from Q4. This should provide strong support to fixed income returns, while aiding equities higher (so long as growth doesn’t slow too much). The underweight to cash allows us to harvest what should be a period of positive (modest) returns across both equities and fixed income.

This month we are adding some risk, moving modestly overweight equities however, fixed income remains our preferred asset class for now.

Fixed income (Overweight +2)—While resilient growth and sticky inflation in the US and Australia have delayed rate cuts until later in 2024, central banks across Europe, the UK and Canada, are trimming rates imminently. With markets sceptical about a cut in Australia before mid-2025, we retain an overweight to local government bonds to capture an earlier start to trimming. Our overweight to credit has continued to perform strongly over recent months, as credit spreads have continued to trend tighter. Renewed tightness and belated signs of macro weakness in the US have led us to trim high-yield credit (from +2 to +1). Despite an expectation that spreads may widen from here, current carry remains attractive.

Equities (Overweight +1)—Falling inflation and policy support, plus only a mild growth slowing, argue against being underweight most markets. Yet, with a ‘soft landing’ largely priced and recent strong returns, there is less support for a large overweight to equities at this juncture. Still, absent a sharp re-acceleration in inflation, any near-term correction in markets is likely to be an opportunity to build positions, rotating from fixed income.

Looking across regions, elevated valuations and concentration risk justify only a neutral stance for US equities, despite strong capex, policy stimulus and thematic drivers associated with the energy transition. The emerging recovery and imminent rate cuts see us close our underweight to European equities. While a rally in China is likely near term, we remain cautious about its sustainability and have stayed neutral emerging markets. We open our new strategic Japan position as a neutral, given recent strong performance and recent concerns about its demand strength. We retain our modest overweight to Australia, reflecting relatively attractive valuations, fiscal and monetary policy easing that buffers the weakening consumer through H2, while the local market should provide some proxy for an improving outlook in China on the back of policy stimulus.

IMPORTANT NOTE

This content has been prepared by LGT Crestone Wealth Management Limited (ABN 50 005 311 937, AFS Licence No. 231127) (LGT Crestone Wealth Management). The information contained in this content is of a general nature and is provided for information purposes only. It is not intended to constitute advice, nor to influence a person in making a decision in relation to any financial product. To the extent that advice is provided in this content, it is general advice only and has been prepared without taking into account your objectives, financial situation or needs (your Personal Circumstances). Before acting on any such general advice, we recommend that you obtain professional advice and consider the appropriateness of the advice having regard to your Personal Circumstances. If the advice relates to the acquisition, or possible acquisition of a financial product, you should obtain and consider a Product Disclosure Statement (PDS) or other disclosure document relating to the financial product before making any decision about whether to acquire it.

Although the information and opinions contained in this document are based on sources we believe to be reliable, to the extent permitted by law, LGT Crestone Wealth Management and its associated entities do not warrant, represent or guarantee, expressly or impliedly, that the information contained in this content is accurate, complete, reliable or current. The information is subject to change without notice and we are under no obligation to update it. Past performance is not a reliable indicator of future performance. If you intend to rely on the information, you should independently verify and assess the accuracy and completeness and obtain professional advice regarding its suitability for your Personal Circumstances.

LGT Crestone Wealth Management, its associated entities, and any of its or their officers, employees and agents (LGT Crestone Group) may receive commissions and distribution fees relating to any financial products referred to in this document. The LGT Crestone Group may also hold, or have held, interests in any such financial products and may at any time make purchases or sales in them as principal or agent. The LGT Crestone Group may have, or may have had in the past, a relationship with the issuers of financial products referred to in this document. To the extent possible, the LGT Crestone Group accepts no liability for any loss or damage relating to any use or reliance on the information in this document.

This content has been authorised for distribution in Australia only. It is intended for the use of LGT Crestone Wealth Management clients and may not be distributed or reproduced without consent. © LGT Crestone Wealth Management Limited 2024.

.png?width=770&height=577)